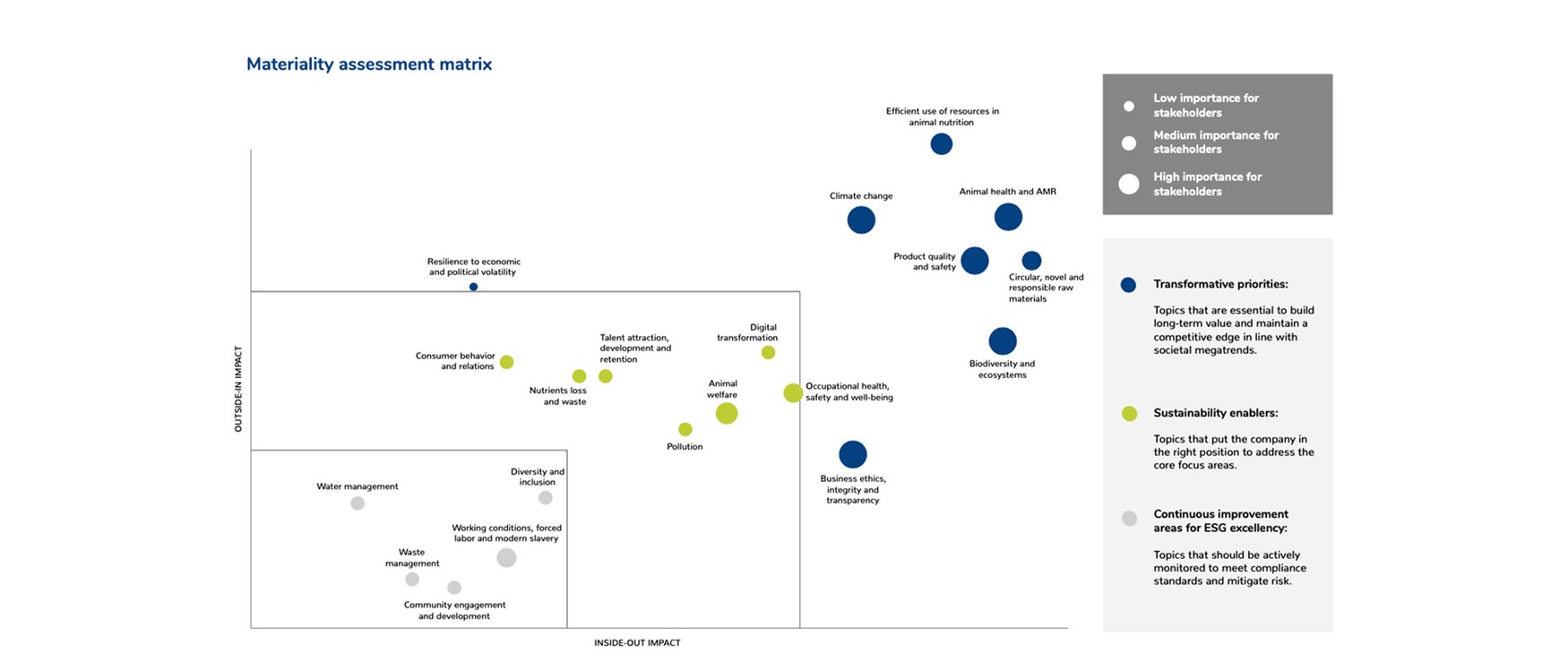

In anticipation of the sustainability reporting requirements outlined in the CSRD, which will be in force for disclosures related to 2024, Nutreco decided to already move forward in 2022 to perform a materiality assessment taking into account the double materiality principle. Double materiality in reporting accounts not only for how a company affects the environment and society but also how the environment and society impact the company's financial value. A sustainability topic meets the criteria of double materiality if it is material from the impact perspective (inside-out) and from the financial perspective (outside-in).